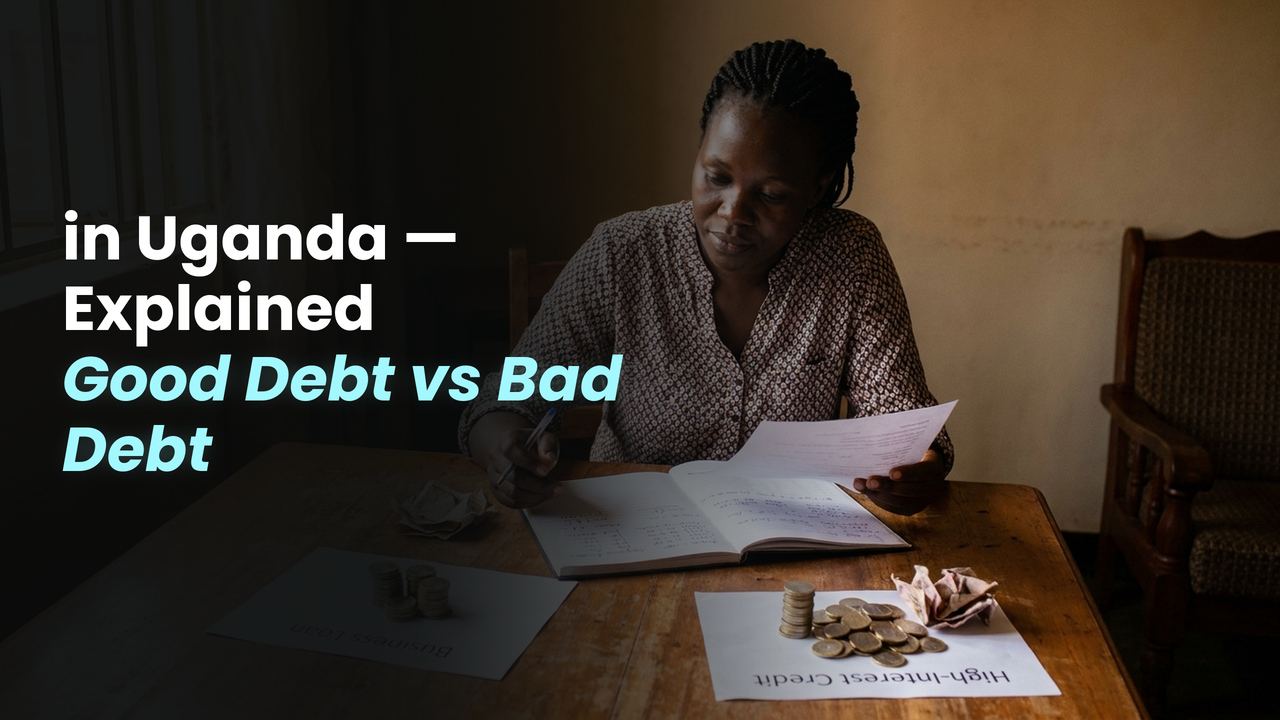

Good debt is borrowing that helps you build wealth, generate income, or improve your financial position over time — such as a business loan that increases your revenue or an education loan that improves your earning potential. Bad debt is borrowing to fund consumption that doesn't create value, like taking a high-interest loan to pay for luxuries or cover avoidable expenses. The key distinction is whether the debt puts money back into your pocket or simply drains it.

No. Borrowing is a financial tool, and like any tool, its impact depends on how you use it. Used strategically, credit allows you to seize time-sensitive business opportunities, manage cash flow gaps, or invest in income-generating activities. The problem arises when people borrow more than they can repay or use loans for non-productive spending. Understanding your repayment capacity before borrowing is the most important step in making debt work for you rather than against you.

Good debt in Uganda typically includes business loans used to buy stock, equipment, or expand operations; SACCO loans used for productive investments; education loans that improve your earning potential; and in some cases, property loans that build long-term asset value. Loans used to generate income that exceeds the cost of borrowing are generally considered good debt, provided the repayment terms are manageable relative to your income.

Ask yourself: will the money I borrow generate more income than the cost of the loan? If you are borrowing UGX 500,000 at a fixed fee and using it to restock a business that earns UGX 900,000 in profit per cycle, the loan is working for you. If you are borrowing to cover daily expenses with no clear repayment source, the loan will likely hurt your finances. Always calculate the total repayment amount and confirm you have a specific income source to repay it before borrowing.

Avoid borrowing more than one loan at a time from different lenders, which creates overlapping repayment pressure. Only borrow what you need and can repay from a known income source. Read all terms carefully — including fees and penalties. Never roll over a loan to cover a previous one without a clear plan. Building an emergency savings cushion, even a small one, reduces the frequency with which you need to borrow for short-term gaps.

Your debt-to-income ratio compares your total monthly debt repayments to your monthly income. For example, if you earn UGX 800,000 a month and your loan repayment is UGX 200,000, your ratio is 25%. Lenders use this to assess whether you can handle additional borrowing. A ratio above 40–50% is generally considered risky. Keeping your ratio low means you retain financial breathing room and are more likely to be approved for future credit when you actually need it.

It depends entirely on how you use it. A mobile loan used to restock your business, cover a medical emergency, or manage a short-term cash flow gap — and repaid on time — is a productive use of credit. The same loan used repeatedly to cover everyday expenses you can't afford suggests a cash flow problem that borrowing will make worse, not better. Mobile loans from apps like Fido are designed for short-term, high-urgency needs, not long-term financing. Use them deliberately.